“I’ll gladly pay you Tuesday for a hamburger today.” — J. Wellington Wimpy, Popeye Comic Strip Character, March 1932

IOUs and Financial Reckonings

In 1932, a cartoon character from the comic strip Popeye named J. Wellington Wimpy perfectly captured the desperation of the Great Depression with a simple request: “I’ll gladly pay you Tuesday for a hamburger today.” His promise hinged on three leaps of faith still central to all finance: that the borrower can pay, that the money repaid will hold its value, and that the borrower will still be around when the bill comes due.

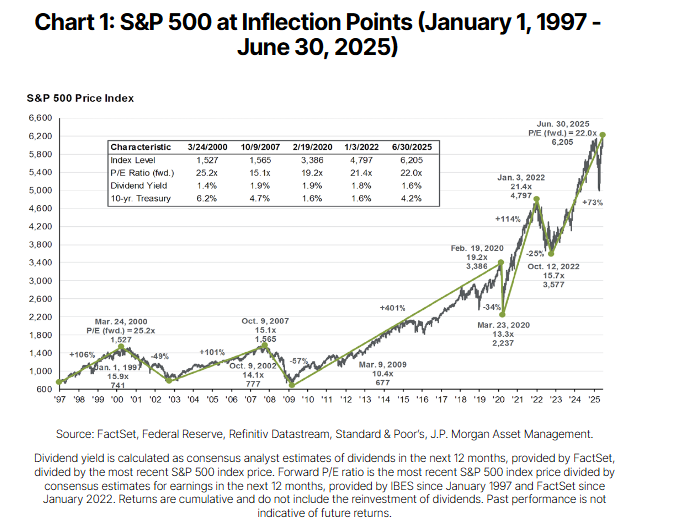

The U.S. government is the world’s largest borrower, and investors who buy its bonds rely on that same collective faith. According to Jeff Krumpelman, Mariner’s Chief Investment Strategist, the market spent the first half of 2025 testing that faith. The S&P 500’s turbulent ride, during which the index fell almost 20% between February 19 and April 8, then rallied about 19% by May 31, eclipsing its prior high by late June, was not a reflection of a failing economy, but of faltering confidence.

Krumpelman notes that while the “hard data,” such as real GDP, earnings, employment, consumer spending, and

business investment, held up well, the market’s tumble was driven by an overly pessimistic reading of the “soft data,” including consumer and CEO confidence surveys, which plummeted after an April 2 announcement of significantly higher tariff duties. This psychology-driven sell-off, he explains, likely caused the S&P 500’s forward P/E ratio to drop from over 22 times earnings to about 18, only to rebound after a confidence-restoring “tariff time-out” (TTO) went into effect on April 8 (see Chart 1).

The TTO appears to have been the spark that ignited a rally of nearly 12% from April 8 through April 30 and which carried the S&P 500 to an all-time high as of June 30. To put it in Wimpy’s terms, the market became less certain about “next Tuesday,” so investors were less willing to pay yesterday’s price for tomorrow’s earnings. When new information came into the market, it didn’t take long for them to change their minds.

During periods of relative stability and almost predictable returns, it’s easy to forget that volatility remains a central feature of markets and investments. Market prices continuously adjust to new information, often overreacting on the upside to perceived good news and selling off sharply on perceived bad news. That price movement can tempt investors to make major shifts in asset allocation, the result of which is whiplash in returns and, ultimately, wealth destruction in a classic sell-low, buy-high scenario.

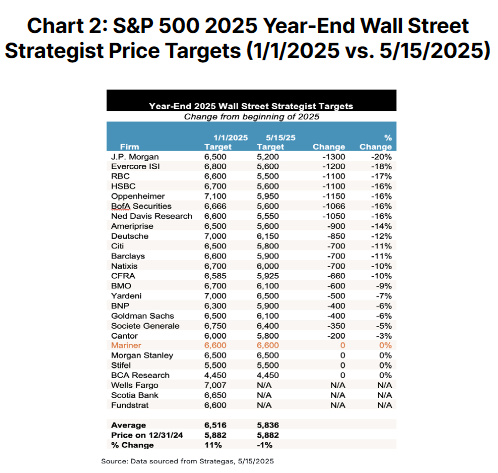

Still, while many firms repeatedly revised 2025 market outlooks, Mariner held its constructive view, arguing that the underlying fundamentals remained neutral to positive throughout this year’s turbulence (see Chart 2).

It may not seem obvious, but the market is forever questioning which of Wimpy’s promises may not hold up. Is it

his capacity to pay? The future value of his dollar? Or whether he’ll even be there on Tuesday? When markets are driven by sentiment, as they so often are, the “hard data” often gives the clearest indication of whether the

borrower’s IOUs can and will be paid.

Mind the Gap

For U.S. investors, the last few decades have proven that focusing on American companies has been a winning strategy. Since the early 1990s, the U.S. weighting in the MSCI All Country World Index has climbed from around 30% to a historically high 64% today. As reassuring as that sounds, there is no guarantee that the trend will continue; market leadership is rarely a permanent position. For several reasons, a compelling, data-driven case for international diversification continues to emerge, built on a clear, significant valuation gap.

As of June 30, 2025, the S&P 500 traded at a forward price-to-earnings (P/E) ratio of 22.0x. While there are valid arguments to be made that the lofty valuation is warranted, as it reflects the growth and dominance of U.S. tech companies, the valuation multiple also represents a sizeable premium relative to other regions. In contrast, markets in the Euro- zone (14.3x), Emerging Markets (12.9x), and China (11.5x) offer substantially lower valuations. For investors, the widening valuation gap points toward the potential for higher future returns from assets abroad that are not as richly priced.

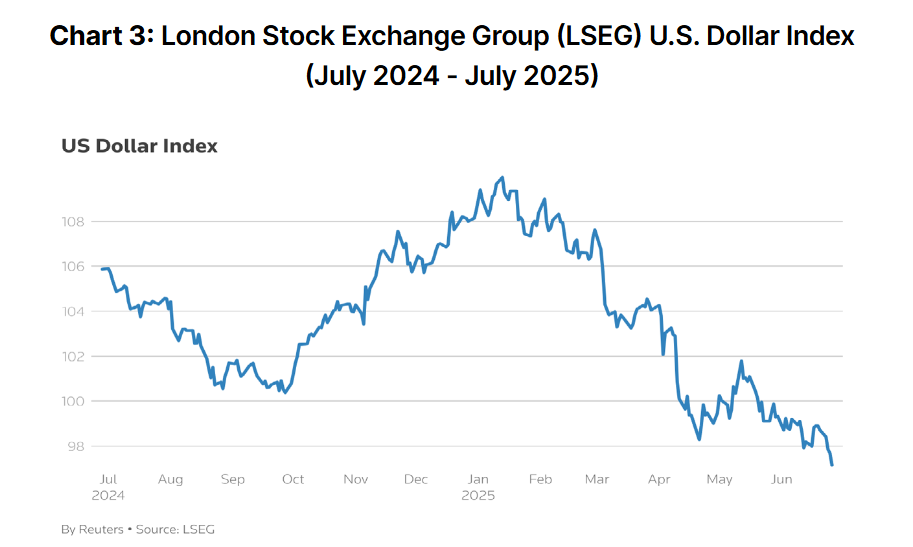

Another key factor in evaluating the risks and opportunities in foreign markets is the currency cycle. For years, a strengthening U.S. dollar has been a headwind for international returns, as foreign profits are worth less when converted back into U.S. dollars. However, after a multi-year run that saw the dollar index peak in late 2022, this trend may be shifting. A weakening dollar would act as a powerful tailwind, boosting the value of international

investments for U.S.-based portfolios.

This rotation may already be in its early stages, as year-to-date through June 30, 2025, the MSCI AC World ex-U.S. Index has returned 9.2%, outpacing the S&P 500’s 6.2% return. Meanwhile, in the first six months of 2025 the U.S. dollar logged its worst first-half performance in more than fifty years, falling more than 10% against a basket of major currencies (see Chart 3), according to Morningstar, largely because of escalating trade-war concerns. While the dollar typically strengthens during eco- nomic turmoil as investors seek safe havens, expectations of interest rate cuts later this year may lower yields, which would be another headwind for the dollar.

In a market of promises, concentrating all one’s faith in a single borrower is a significant risk, no matter how reliable they’ve been. Diversifying even a modest slice of a portfolio into global equities may be a practical step to ensure performance isn’t tethered to a single economy’s fate. Consider minding the valuation gap, watching the currency winds, and recognizing that next “Tuesday’s” hamburger payment could arrive from a continent away.

Chart 1 Source: am.jpmorgan.com, June 30, 2025

Chart 2 Source: marinerwealthadvisors.com, June 6, 2025

Chart 3 Source: reuters.com, June 27, 2025

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for your clients. All performance referenced is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly. The S&P 500 is a capitalization-weighted index designed to measure the performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The MSCI All Country World Index (MSCI ACWI) is a free-float weighted equity index that includes both developed and emerging market countries. The MSCI AC World ex-U.S. Index captures large and mid cap representation across 22 developed markets and 26 emerging markets countries, excluding the United States. The MSCI Eurozone Index captures large and mid cap representation across 10 developed markets countries in the Eurozone. The MSCI Emerging Markets Index captures large and mid cap representation across 26 emerging markets countries. The MSCI China Index captures large and mid cap representation across China A-shares, H-shares, B-shares, Red chips, P chips and foreign listings. The U.S. Dollar Index (DXY) measures the value of the U.S. dollar relative to a basket of foreign currencies. Economic and market forecasts set forth may not develop as predicted. Investing in stock includes numerous specific risks, including potential loss of principal. Investing in foreign and emerging markets securities involves special additional risks, including currency risk, political risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks. Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. No strategy assures success or protects against a loss. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price. Diversification and asset allocation strategies do not guarantee profits or protection against loss. Investments in securities and other instruments involve risk and will not always be profitable. Loss of principal is possible. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.